26 Feb 2026

Racing the clock: how project controls keep data center delivery on time and on budget

Cost estimation and project controls are frequently treated as distinct disciplines: one focused on pricing, the other on performance tracking. But in practice, the two are deeply connected. This article explores why project controllers can’t afford to ignore the estimate, how misaligned structures hurt control, and what steps can be taken to bridge the gap from estimate to budget. A must-read for anyone involved in project cost control, even if they’re not doing the estimating themselves.

In project management world, it’s common to draw a line between cost estimation and project controls, with project controls professionals often stating that cost estimation is not part of their job. While both aim to support project planning and data-driven decision making, they are distinct disciplines, each requiring a unique mindset and skillset.

This difference may be difficult to understand at first, but the differences lie in four critical areas:

While it is easy to draw these differences in theory, in practice, the line between these roles is far blurrier than it appears. Nowhere is that more evident than in the process of transforming a cost estimate into a structured project budget.

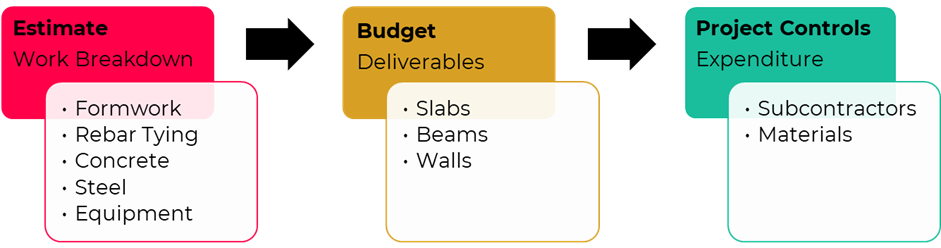

For project controls professionals, the cost estimate is more than just a pricing output: it’s the foundation of the project budget. But here’s the catch: the estimate, in its original form, is rarely suitable for cost tracking. It’s often too detailed, fragmented, or built around commercial logic that doesn’t reflect how the work will actually be executed or how costs are recorded in the ERP.

Field teams report progress against physical deliverables like slabs, beams, or walls — not individual construction activities such as formwork or rebar tying. Meanwhile, vendors invoice based on broader scopes such as concrete works — not the discrete components found in the estimate. And ERP systems track expenditures using cost account structures, not estimating line items.

That’s why the project budget must act as a bridge, connecting the granular logic of the estimate to the control structures used in the field and in enterprise systems. Without that connection, traceability is lost, forecasting becomes unreliable, and cost control suffers.

The golden rule? If you can’t trace a cost from budget to actual to forecast, your control system is weak.

Too often, estimators develop estimates from a purely commercial perspective, and the project cost controller inherits a structure that doesn’t align with control needs. The result? Manual rework, time loss, and a breakdown in traceability.

In practice, conforming the Estimate into a Budget (often referred to as recasting) will always occur, to align the cost structure with how physical progress will be measured on site, and how actual costs will be collected. Returning to the earlier example of concrete works, while the estimator may break down into its detailed tasks, the project controls engineer will aggregate those details into measurable deliverables and then capture the costs at an even higher level, potentially under a single line of concrete works. The real question is not whether recasting is needed, but rather how complex the recasting activity must be.

The fix is simple in theory but challenging in practice: collaboration from day one. When project controls professionals engage early, they can help shape a structure that both reflects the estimator’s commercial logic and supports downstream cost control.

Project cost controllers may not own the estimate, but they do own its usability. That means getting involved early in the estimation reviewing process — not to influence prices, but to ensure that the estimate structure will map effectively to the budget and the company-wide cost account framework. The estimator draws the roadmap — but it’s the project cost controller who makes sure the project stays on course.

It also means advocating for (and using) tools that bridge the gap between estimate and control. Regardless of the integrated platform, the goal is the same: ensuring traceability from estimate to budget to actuals.

In future posts, we’ll explore some of the tools and practical strategies that help make this integration smoother and more scalable.